After a period of unstable politics, frail finances and flagging growth, Mongolia may be turning a corner

A PHRASE is repeated like a mantra around Ulaanbaatar, the steppe capital: “Mongolia is back in business.” The prime minister, Chimed Saikhanbileg, has said it several times. Foreign mining executives and diplomats have also taken up the refrain. And there is something tangible to cheer at last. After years of squabbles and delays, development of the Oyu Tolgoi copper and gold mine in the Gobi desert, by far Mongolia’s biggest investment project, seems to be back on track with the signing on December 15th of a new financing package worth $4.4 billion.

A Mongol hoard

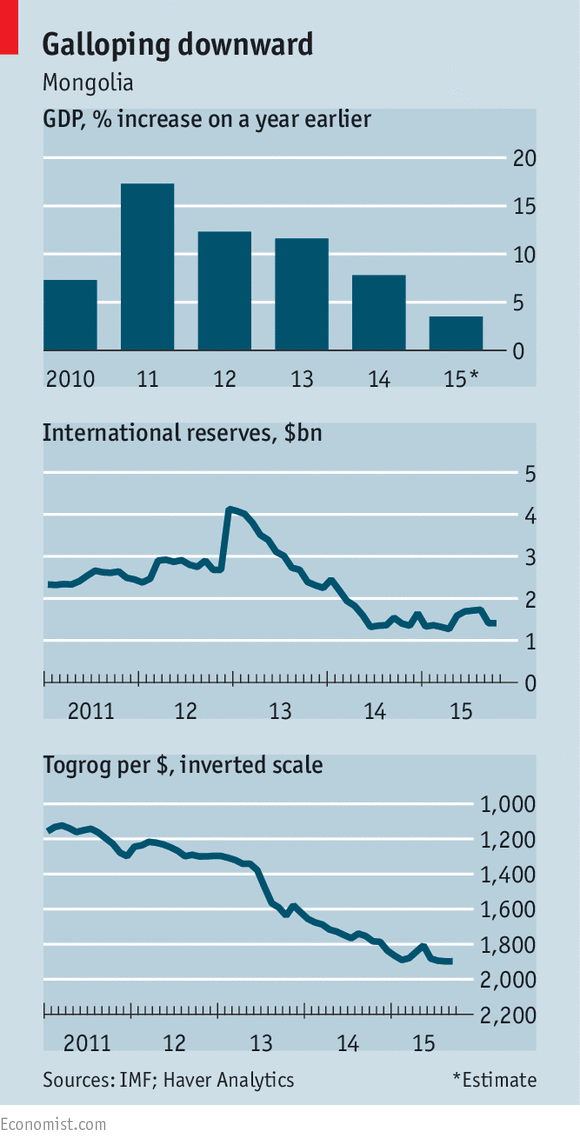

It is certainly welcome news after a period of spectacular mismanagement, both of the economy and of relations with foreign investors, by the coalition government led by the Democratic Party. In 2013-14 the government introduced disastrous steps to counter a slump in growth that a couple of years earlier had peaked at 17% (see chart). Measures to stabilise prices and subsidise mortgages involved huge injections of central-bank money and off-budget financing. Bad loans in the banking system ballooned. The currency, the togrog, slumped. Foreign-exchange reserves shrank. A balance-of-payments crisis loomed. Mongolia had to turn to China, its overbearing neighbour, for help.

Most inept of all, the government fell out with Oyu Tolgoi’s foreign investors just as worldwide commodities prices were tumbling. The mine, boasting a copper deposit that is among the world’s biggest and purest, is controlled by Rio Tinto, a British-Australian firm, with the Mongolian government holding a 34% stake. The open-pit portion of the mine began operating in 2013 and has already produced 1.5m tonnes of copper concentrate, most of it for China. But four-fifths of the project’s value may lie underground.

This week’s financing deal, which involves 15 commercial banks and the American, Canadian and Australian export-credit agencies, will allow work to begin on the underground mining phase. When it is at full tilt, Oyu Tolgoi may account for a third of Mongolia’s entire economy. No wonder that the protracted squabbling between Rio Tinto and Mongolia over taxes, management fees and other issues seemed like a bad omen. Foreign direct investment in Mongolia fell by 85% between 2012 and 2015. But now the new package is a “huge milestone”, says America’s ambassador to the country, Jennifer Galt.

Mongolia is not out of the woods yet. Hard currency remains in short supply, inflation is stubbornly high and the budget deficit is way above the target of 2% of GDP, despite tax rises and cuts in public-sector pay. Above all, the country’s political turbulence is all but certain to continue. The government’s fragility was laid bare in August when the Mongolian People’s Party, the country’s former communists, was ejected from the coalition and six cabinet ministers were replaced.

A new round of parliamentary elections takes place next spring. According to Sumati Luvsandendev of the Sant Maral Foundation, an independent polling outfit, ineptitude and squabbles within the Democratic Party have led its approval ratings to decline “quite dramatically”. Mr Sumati predicts solid gains for the Mongolian People’s Party.

The party will appeal to Mongolians’ sense of nationalism over mining. One of its MPs, Sodbileg Otgonbileg, says that the Democratic Party’s hopes of winning public applause for the Oyu Tolgoi deal are misplaced. Rio Tinto, he says, has been allowed to get away with too much control, excessive management fees and procurement irregularities; instead of maximising the benefit for Mongolians, it is saddling them with debt—“as if we own a beautiful apartment but get treated like a squatter”. Activists are critical, too. Sukhgerel Dugersuren of OT Watch, an NGO, says the mine’s use of the area’s scarce water is unsustainable. She says the mine pays too little tax—and inadequate attention to the interests of local herders.

Executives at Rio Tinto and Oyu Tolgoi insist that the project is run to the highest international standards, that 95% of its workforce is Mongolian and that it has already paid $1.3 billion in taxes and other fees to the Mongolian government, with much more to come as production increases. They also expect copper prices that are depressed by a sharp drop in Chinese demand to recover by the time the mine’s underground phase is ready to produce. And the executives have faith that, whatever the outcome of the election next spring, Mongolian resource nationalism will be kept in check and the project will remain resolutely on track. Indeed, they repeat it like a mantra.

Source:Economist.com

0 comments:

Post a Comment